By Gene Balas, CFA®

Investment Strategist

When positioning portfolios for what may be a period of rising interest rates, the obvious solution may seem to be putting the funds in short-term instruments, or perhaps to instruments with floating rates that can increase in tandem with any rise in interest rates. Certainly, there may be a strong case to be made for allocating at least some of your assets to floating rate notes. But why not earmark all of your fixed income holdings to floating rate instruments if bond prices continue to get crushed in this environment?

There are more than just a few things to unpack in this seemingly simple solution. First of all, it’s hardly a secret that the Fed is intent on hiking interest rates. Investors are well aware of what’s coming—so much so that, arguably, some of these rate hikes may have already been priced into bond yields, having sent bond prices lower, as painful as that adjustment may have been.

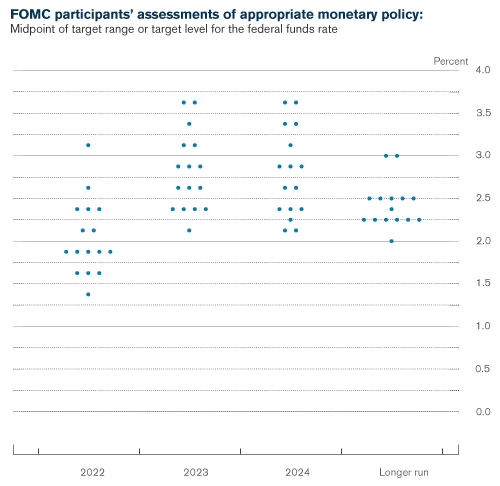

But how high will the Fed ultimately hike rates? Even members of the Federal Reserve’s rate-setting Federal Open Market Committee (FOMC), haven’t shown widespread consensus. Consider the adjacent graph, known as the ‘dot plot,’ which depicts where each member of the FOMC views rates during 2022, 2023, 2024, and over the longer run. Each individual member’s view on the level of rates is represented by a dot on the chart (members are not identified by name).

Source: Source: Federal Open Market Committee (FOMC).

Note: Each shaded circle indicates the value (rounded to the nearest 1/8 percentage point) of an individual participant’s judgment of the midpoint of the appropriate target range for the federal funds rate or the appropriate target level for the federal funds rate at the end of the specified calendar year or over the longer run. One participant did not submit longer-run projections for the federal funds rate.

You’ll note there’s quite a wide range of viewpoints! In 2023 alone, one Fed member sees the Fed funds rate just a bit above 2%, while a couple see it above 3.5%, with the rest evenly spread out across the middle of that range. One key reason for such a wide range of expectations is the extreme amount of uncertainty for the future. We simply don’t know:

- How long high inflation would persist on its own (absent any Fed intervention),

- How well inflation might respond to the recent and expected future rate hikes, or

- How geopolitics (such as the Russia-Ukraine war) could affect the economy and bond yields.

We also need to consider that high inflation itself can be the master of its own demise. There’s no question that the surge in prices we have seen is due in large part to supply that is constrained, combined with strong consumer demand, such as from a collective pent-up desire to return to ‘normal’ life.

High prices, however, can help to stifle demand. This is especially the case when real hourly earnings, as reported by the Bureau of Labor Statistics, fell by -2.6% in the twelve months through April 30th. In other words, consumers’ incomes, on average, are shrinking after adjusting for inflation. It’s hardly an environment that’s conducive to consumers continuing to shop with abandon. And if they cut back on spending, that can slow down the economy and reduce the need for as many rate hikes.

Plus, tighter financial conditions aren’t solely determined by how high interest rates go. They also tighten when financial asset prices (like those of stocks) fall. The current stock market correction—especially if it’s sustained—can do some of the Fed’s work for it, by making money less readily available.

Looking ahead

We’ve touched on just a few of the moving pieces involved in inflation and interest rate dynamics. The bond market attempts to consider all of these factors when setting prices and determining yields across the spectrum of maturities, credit qualities, and fixed income sectors. Of course, the base case view is that interest rates are likely to rise, but there remains considerable uncertainty over just how high, how soon, and how long higher rates might last.

If inflation slows quickly because supply comes back online (e.g., people re-enter the labor force, markets overseas including China rebound from Covid concerns, supply chains are restored, etc.), or if inflation slows instead because demand drops considerably, the Fed may not need to hike rates as much. And if the economy slows, or geopolitical concerns mount, then bond yields might not go as high as some may fear. Keep in mind that any significant geopolitical developments can send investors globally into the safe haven of Treasuries, pushing yields down. This may especially be the case considering how much longer-term bond yields have already risen.

Long story short, we believe bond investors would be prudent to diversify across sectors and styles rather than allocating 100% of your fixed income portfolio to a single strategy like floating rate debt or short-duration instruments. A distinction can be made, however, between top-down views applied at the portfolio level and security selection decisions made by the managers we utilize.

For the top-down views in our discretionary portfolios, we remain underweight duration while tilting towards ‘unfixed’ income that has the potential to perform relatively better in a rising rate environment. Within the components of each of the ‘sleeves’ of a fixed income allocation, we continue to advocate for active management, believing that skilled managers can more effectively navigate ongoing uncertainty. These managers are well-attuned to what is happening in the economy, geopolitics, inflation, and the markets, so that they can adapt and adjust the portfolios they manage. It’s impossible, however, to avoid market forces entirely.

But remember that there is a reason for diversification: nobody can be absolutely certain any given outcome will occur at some point in the future. Therefore, it may be best to have several active managers who can be flexible enough to accommodate the nature of the flux and uncertainty that now dominate the market, within the confines of the mutual funds they manage.

And while we can make changes in the asset allocations within the fixed income components to reflect current conditions (such as moving assets into floating rate notes), it’s arguably even better to combine that approach with not just one, but several, active fixed income mutual fund managers.

Don’t forget that previous chart showing the diversity of opinion among Fed officials as to where the rates (ones that they control) will be over coming years. Even for Fed officials, it’s hard to have an accurate crystal ball in this environment. For our fixed income strategies, having several different approaches, from several different managers, is an encapsulation of the uncertainty we all currently face. Although it has certainly been a challenging year for bond investors, we believe owning a diversified fixed income strategy may provide you a higher likelihood of success going forward.

The information contained herein is for informational purposes only and should not be considered investment advice or a recommendation to buy, hold, or sell any types of securities. Financial markets are volatile and all types of investment vehicles, including “low-risk” strategies, involve investment risk, including the potential loss of principal. Past performance does not guarantee future results. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio in any given market environment; it is a method used to help manage investment risk. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors. In general, the bond market is volatile, bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. The investor should note that vehicles that invest in lower-rated debt securities (commonly referred to as junk bonds) involve additional risks because of the lower credit quality of the securities in the portfolio. The investor should be aware of the possible higher level of volatility, and increased risk of default. For details on the professional designations displayed herein, including descriptions, minimum requirements, and ongoing education requirements, please visit signatureia.com/disclosures.

Signature Investment Advisors, LLC (“SIA”) is an SEC-registered investment adviser; however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SIA. SIA is a subsidiary of SEIA, LLC, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, 310-712-2323, and its investment advisory services are offered independent of Royal Alliance Associates, Inc. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products or services referenced here are independent of Royal Alliance Associates, Inc.