By Sam Miller, CFA®, CFP®, CAIA®

Senior Investment Strategist

Chinese stocks have continued to sell off in recent weeks in response to a regulatory crackdown targeting a number of key industries. They’re now firmly in ‘bear market’ territory, defined as a 20% drop from a recent high. What started with the pulling of the Ant Financial IPO late last year, quickly evolved into anti-trust regulation against Alibaba and other tech firms—and more recently has targeted for-profit education providers and meal-delivery companies.

Essentially, the Chinese government is concerned about many of the same issues we are facing here in the U.S: competition, consumer rights, protecting small businesses, anti-monopoly practices, data protection, national security, and inequality. Understandably, this ongoing situation has many investors concerned about the world’s second largest economy—uncertain as to what the government’s next steps might be.

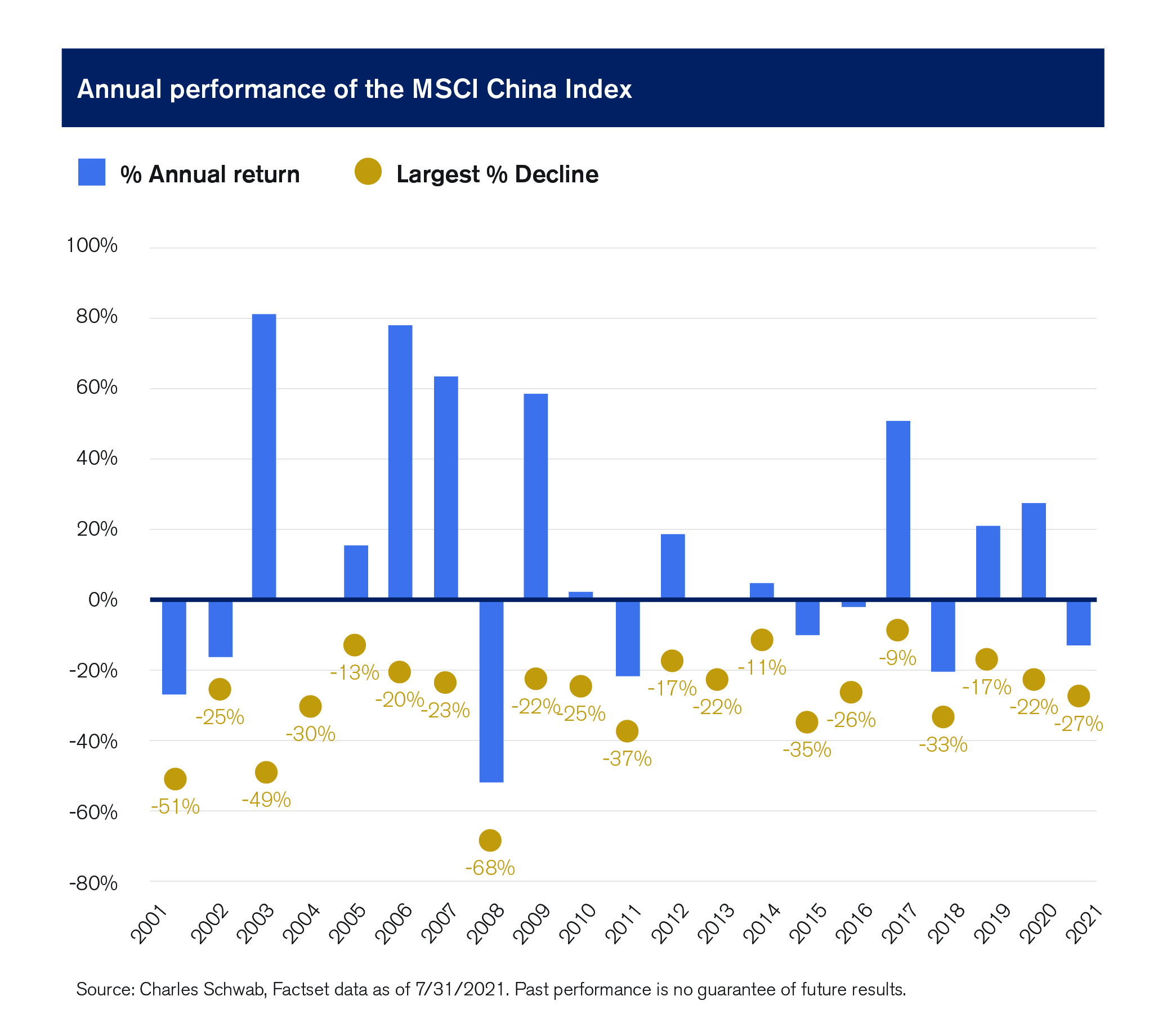

It’s important to remember, however, that investing in China’s stock market has historically come with both high volatility and high returns. Investors have tended to be compensated for this heightened volatility with double-digit annualized total returns over the past 20 years. From 7/30/01 to 7/30/21 the MSCI China Index has delivered an annualized total return of 11%[1]. Of course, market drawdowns are never enjoyable in the moment. But they often present tremendous opportunities for higher future returns going forward. Using history as a guide, we quickly see that the current drawdown is well within the realm of reasonable expectations for China.

Why Should I Bother Owning Stocks Outside the U.S?

For the ten-year period ending June 30, 2021, the S&P 500® Index had an annualized return of 14.84% while non-U.S. Developed stocks (represented by the MSCI World ex-USA Index) generated a modest 5.7%, and Emerging Markets stocks (represented by the MSCI Emerging Markets Index) rose by even less at 4.28%.[2] Given this dramatic outperformance over the last several years, investors may naturally be reconsidering the benefits of investing outside the U.S.

But while non-U.S. equities may have delivered disappointing results recently, it’s important to remember that investing globally provides invaluable diversification benefits. Keep in mind that the U.S. stock market represents roughly 57% of global market capitalization[3]. That means a portfolio invested solely within the U.S. will be missing out on nearly half of the world’s companies.

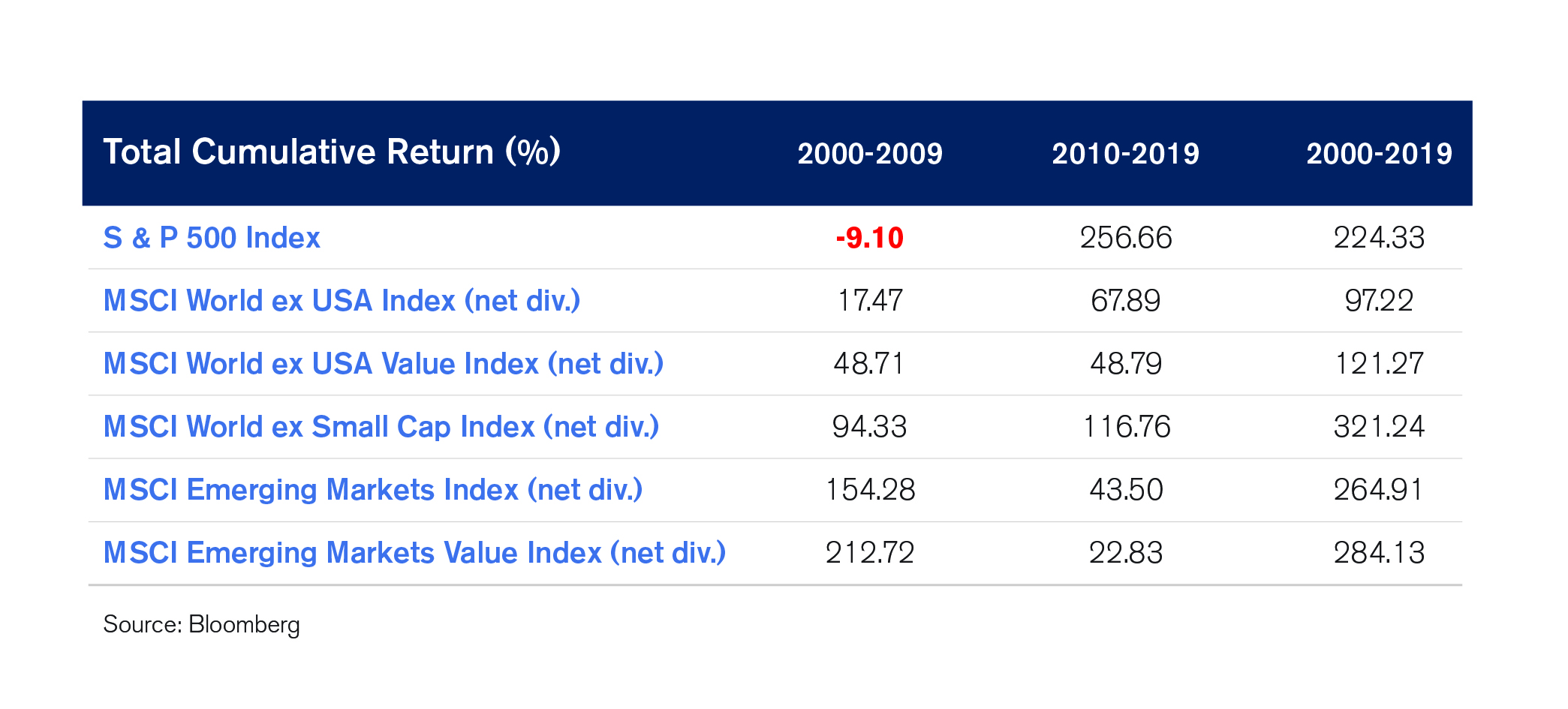

Looking back, the ‘Lost Decade’ (2000-2009) is a great example of the opportunity cost associated with not investing globally. From January 2000 to December 2009, the S&P 500 Index had a cumulative return of -9.10% (its worst ever 10-year performance), largely attributable to the tech bubble and the financial crisis. During that same decade, however, we see that investors who had exposure to other areas of the global landscape were well rewarded with positive returns (see table below).

The benefits of maintaining a globally diversified portfolio—especially a portfolio that targets areas of the market with higher expected returns—is clearly reflected in the cumulative performance data from January 2000 – December 2019. Longer time frames significantly increase the likelihood of having a positive investment experience.

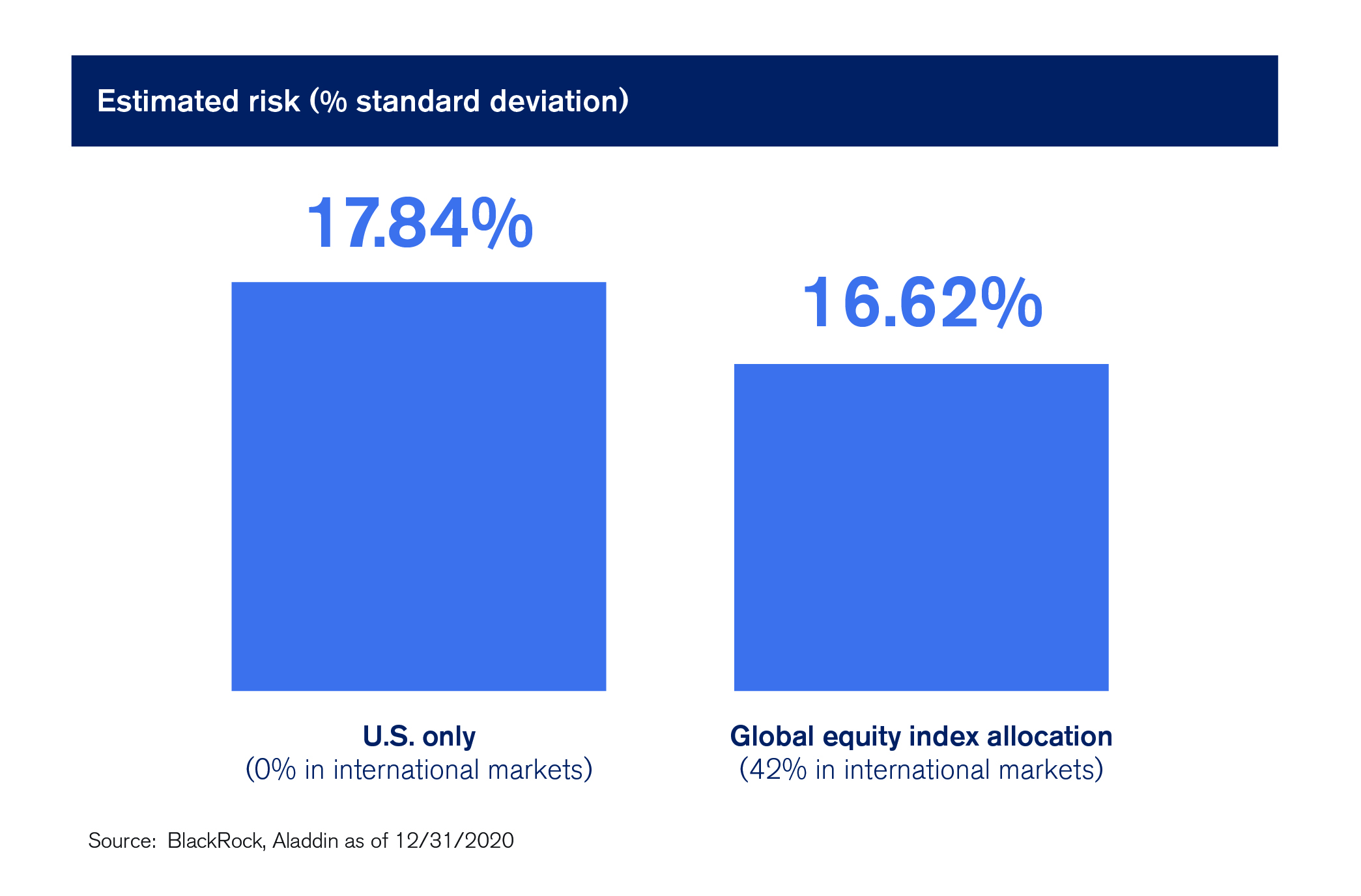

But isn’t investing globally more risky? A common misconception is that international developed stocks and emerging market stocks would make a portfolio riskier. But as the following graphic indicates, the fact that international and emerging market stocks don’t necessarily correlate to the U.S. stock market can actually reduce the volatility of your portfolio over the long-term.

How Should Investors Approach China?

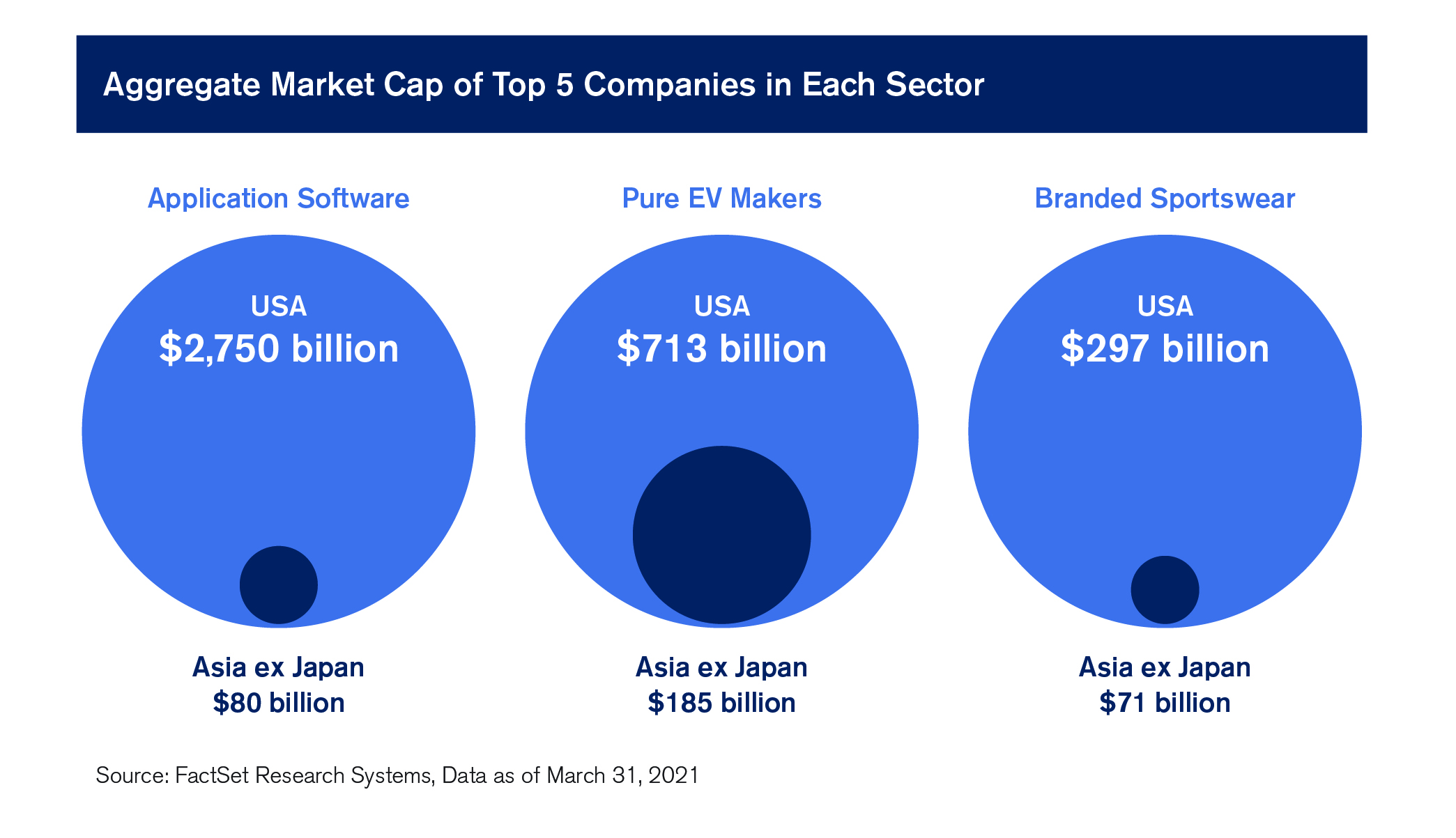

Unlike previous years, this recent drop in Chinese stocks is tied to regulatory uncertainty rather than economic uncertainty. While these pressures may persist for some time (and impact a variety of industries), they should eventually ease. At the end of the day, the potential scope of wealth creation in Asia and its trajectory of discretionary spending, especially in China, is too large to ignore. To put Asia’s total addressable market into perspective, keep in mind that Asia has approximately 7x the population of the Eurozone. And this workforce (Asia ex-Japan) is growing its wages at an average of 7% annually which in turn is driving consumer spending growth by more than 5% annually. These positive trends should fuel the potential for upside—especially in industries driven by innovation like software and electric vehicles (see below).

Regulatory uncertainty has been a fact of life of investing in emerging markets (including China) for a very long time; and it’s likely to remain so for the foreseeable future. While there’s considerable short-term uncertainty, we continue to believe that it makes a great deal of sense to include international and emerging markets as part of a well-diversified portfolio.

[1] Bloomberg

[2] Morningstar

[3] MSCI

For details on the professional designations displayed herein, including descriptions, minimum requirements, and ongoing education requirements, please visit www.signatureia.com/disclosures/. Signature Investment Advisors, LLC (SIA) is an SEC-registered investment adviser; however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SIA. SIA is a subsidiary of SEIA, LLC, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, (310) 712-2323, and its investment advisory services are offered independent of Royal Alliance Associates, Inc. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products or services referenced here are independent of Royal Alliance Associates, Inc.