By Gene Balas, CFA®

Investment Strategist

Stocks or other vehicles with extremely high dividend yields can seem quite tempting. But two words of advice: “Buyer beware.” First, though, what do we mean by “exceptionally high” when it comes to dividend yields? There are, of course, many stocks and other investments that pay attractive dividend yields and are high quality investments. However, yields that are, say, a couple percentage points higher than those of other, comparable investments in the same category are unusual – and that very-high yield is usually due to unique factors particular to that specific company or instrument.

More to the point, there is likely a reason why those yields on those particular securities are so much higher than comparable investments, and those reasons are often not necessarily beneficial. The concept generally applies to most things in life that seem too good to be true – and especially when it comes to investment opportunities.

First, dividends are by no means guaranteed. Most companies can cut them at any time – aside from certain types of preferred stocks, most companies often have wide latitude of what dividend they choose to pay each quarter. Meanwhile, for those vehicles that own a pool of underlying investments, such as loans or mortgages, it may turn out that those investments no longer provide the income stream or security of principal that was once thought, leaving less to return to investors.

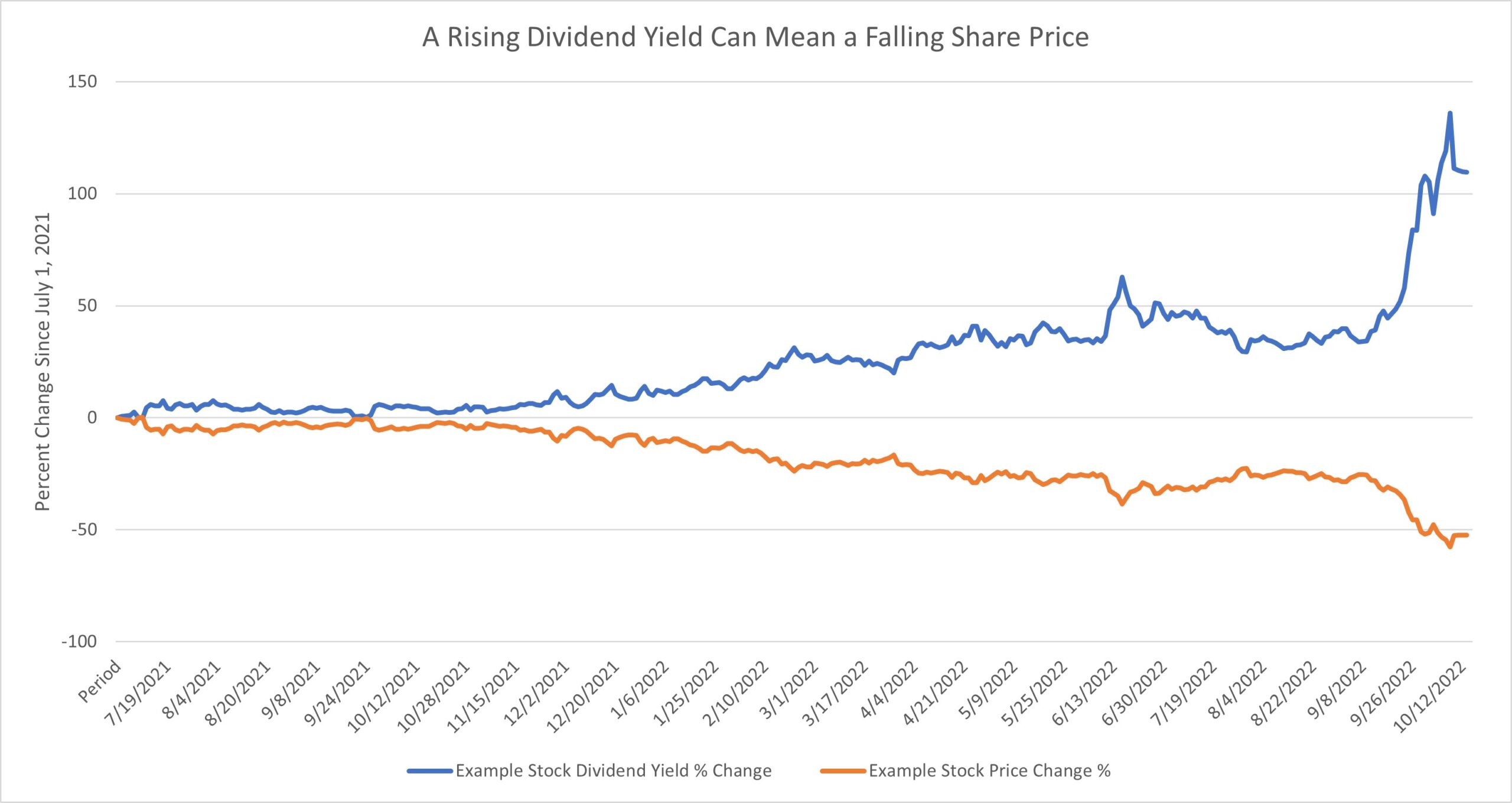

And remembering that yield is the dividend divided by the price, note that a high dividend yield may not be a good sign: It could be a sign that a company or investment is viewed by the market as in some state of current or potential future distress: That means a marked-down share price – and thus, a high dividend yield.

Consider the nearby graph, which shows exactly what is meant when a falling share price means a higher dividend yield. And we certainly would want to consider why the share price has fallen!

Source: Y-Charts. Example using a mortgage REIT for illustration purposes

Furthermore, investments that are priced based on yield, dividend or otherwise, are vulnerable to rising rates: As rates on risk-free assets, such as Treasuries, increases, the market demands more yield (and thus, a lower price) on all other yield-bearing assets.

A combination of rising interest rates and a slowing economy – which is what we are currently facing, with rate hikes by the Fed to combat inflation now triggering worries about a resultant economic contraction – can be deadly for some entities.

In addition to considering what exceptionally high dividend yields mean more generally, we can also consider a couple different examples of types of vehicles, some of which currently sport high yields. They may initially appear attractive, at least until caution prevails. Among these two examples to delve into more detail are business development companies and mortgage REITs.

As one example, business development companies invest in young, untested companies and provide them funding for growth. Some of these vehicles own loans made to those early-stage companies that pay a variable, floating rate, which will increase as the Fed hikes rates.

Thus, these companies will then face higher interest expenses at the same time that their revenues may weaken in tandem with slower economic growth. Remember: the goal of the Fed’s rate hikes is explicitly to slow the economy enough to tamp down inflation. Simply because a loan is higher up in one of these borrower’s capital structure is of no protection if a company defaults anyway.

Likewise, mortgage REITs may face the same problem from borrowers; namely, homeowners who may be seeing their property values sag as mortgage rates go up, and end up underwater on their mortgage. The Fed stated that housing prices have gone up too far, too fast, and that higher mortgage rates are the cure that can restore affordability in housing by lowering home prices (and thus, ease inflation in the process). Lower home prices and higher mortgage rates can mean greater defaults by borrowers, if they cannot sell their home for enough to pay off any delinquent mortgage debt.

Specifically, in the press conference following the Fed’s rate decision September 21, Fed Chair Jerome Powell said the hot US housing market probably has to “go through a correction” to get to a better balance. The Fed chair said that over the longer term what’s needed is for “supply and demand to get better aligned”. In other words, lower (and thus, potentially more-affordable) housing prices are arguably one of the Fed’s goals in its rate-hike campaign to ease very high inflation.

Furthermore, mortgage REITs buy mortgages by using borrowed money, and the intention is to attempt to profit by borrowing at what are usually lower short-term rates to invest in mortgages that are paying what are usually higher rates further out on the yield curve.

However, in the current environment, the yield curve is inverted – the short-term rates that these mortgage REITs are paying are higher than the long-term rates than they are earning. In other words, some mortgage REITs are operating at a loss in the current environment just on the spread of short-term vs. long-term interest rates alone. And that doesn’t even factor in the point above, about mortgage-holders defaulting on their debt, nor does it include all the other expenses such vehicles incur as a regular part of their business.

Thus, upon closer examination, high dividend yields may not represent an opportunity – they may instead be a warning.

The information contained herein is for informational purposes only and should not be considered investment advice or a recommendation to buy, hold, or sell any types of securities. Financial markets are volatile and all types of investment vehicles, including “low-risk” strategies, involve investment risk, including the potential loss of principal. Past performance does not guarantee future results. For details on the professional designations displayed herein, including descriptions, minimum requirements, and ongoing education requirements, please visit www.signatureia.com/disclosures. Signature Investment Advisors, LLC (“SIA”) is an SEC-registered investment adviser; however, such registration does not imply a certain level of skill or training and no inference to the contrary should be made. Securities offered through Royal Alliance Associates, Inc. member FINRA/SIPC. Investment advisory services offered through SIA. SIA is a subsidiary of SEIA, LLC, 2121 Avenue of the Stars, Suite 1600, Los Angeles, CA 90067, 310-712-2323, and its investment advisory services are offered independent of Royal Alliance Associates, Inc. Royal Alliance Associates, Inc. is separately owned and other entities and/or marketing names, products or services referenced here are independent of Royal Alliance Associates, Inc.